BANKING AND MONEY IN JAPAN.

PART I.: THE BANKING SYSTEM.

CHAPTER I.: COMMON BANKS.

SECTION I.: EARLY METHODS.

NOTHING definite is known about the banking system of the early days of Japan; but it is clear that the system played no important part in affairs, since the insignificance of trade and industry called for no extensive credit arrangements, and the spirit of contempt for business was general. That sentiment was the result of the preference given to agriculture as the sole source of national wealth, and was also encouraged by the reign of feudalism, which was universal. The class of people who were esteemed were the Samurai (vassals), while tradesmen, artisans, and mechanics were held as of little account. Money was regarded as the ugliest of all things; and even to handle it was thought to pollute the hand of the Samurai. Little protection was given to the money-changers, the rate of interest was fixed by strict enactment, and the debtor was the more favored party. By force of so-called Tokusi (merciful laws), after a certain term the creditor was obliged to surrender the right of demanding payment, and often accumulated wealth was made the object of compulsory public contribution. With such a state of things, it is evident that banking could not make much Edition: current; Page: [410] progress, and the business of pawn-lending was done largely in secrecy. Strangely enough, blind men were often engaged in this business. However, even then the system of money-lending was tolerably well developed. In the fifteenth century (1433 ad) an edict was issued which decreed that:

(1) Articles of daily use may be pawned, but the term for wearing apparel is limited to a year, and that for weapons to two years.

(2) The rate of interest must be within fifty per cent.

(3) Those who do the business without sufficient funds shall be punished, and if they abscond, the liability must be borne by the people of the district.

Taking advantage of their not being under the care of the Government, ruffians seem to have often plundered the pawnbrokers, and a law was enacted in 1538 ad to punish those outlaws. In 1544 ad, the maximum rate of interest was lowered to twenty per cent. against pledges, and to thirty per cent. without pledges. In the famous “Hundred Clauses” of 1790 ad we find:

(1) Pawned goods can be sold after the lapse of eight months.

(2) Those who sell the goods pledged, regardless of the payment of interest within the term, will be heavily punished.

Associations of pawnbrokers were formed to facilitate the exercise of administrative control, and those have been continued to the present time. Indeed, the work done by pawnbrokers is really enormous. Almost in every village, there is one or two of them granting credit to poor people upon various domestic utensils and implements as pledges. Formerly, their places of business were indicated by a peculiar signboard; now they are generally marked out by black curtains hung in the entrance. There are central establishments, which do a large business by repawning for the smaller houses. At present, the term at which the pledge may be sold is six months, to be shortened or prolonged by special contract. In case of the loss of the pledged goods by fire or theft, the pawnbroker loses the money lent, and the owner the goods. Loss by the processes of nature is to be borne by the latter. The rate charged is one per cent. per month for sums below thirty-five cents, four per cent. per month up to one yen; three per cent. for less than five yen; two and a half per cent. for ten yen. By such means, the lack of a proper banking system has been, to a large extent, supplied.

USURY LAWS.

The enactment of usury laws is very old. In the first year (687 ad) of the reign of the Empress Jito, those who paid back a debt by labor were freed from the obligation to work for the interest. In the fourth year of Emperor Temmu (676 ad), the maximum rate of interest was fixed at one hundred per cent. in the case of ordinary loans, and at fifty per cent. in the case of money lent by the Government. It was also prohibited that the debtor should pay with his labor after the sale of his property had proved insufficient to Edition: current; Page: [411] cover the debt. Many enactments to the same effect were issued subsequently. In 1591 ad, ten merchants in Nava were executed because they not only exacted usurious rates, but traded on a borrowed fund. In 1744 ad, the number of so-called Fudasashi was limited to one hundred and nine, and the rate they could charge was less than fifteen per cent. Fudasashi were originally keepers of a waiting-place in front of the Government storehouse, from which the feudal vassals received their salary, paid mostly in rice. As the disbursement took some time, the vassals delegated to them the right of receipt. Gradually something like a discounting of these “rights” began; the keepers buying the “right” at a discount and getting the payment from the storehouse. This business became very lucrative, and some of the Fudasashi became very wealthy. They went so far as to lend the vassals money, receive their deposits, and borrow from other firms in the same business. The Exchequer lent to them on pledges worth two and a half times the amount of the loan, with interest at five per cent. A regular staff was employed by them, including chief manager, negotiator, rice examiner, list-maker, accountant, writer, receiver, and clerks. But the peculiarity lay in the fact that the actual manipulation of money was done as a matter of necessity by the head of the firm. The following books were kept by these people:

(1) The big book (Ochio), wherein were written the name, salary, and debts of the customers; (2) the cheque-book (Kitte chio), containing the payments and receipts of money and rice; (3) the rice account (Ki ri mai chio), in which the amount to be claimed from each customer was minutely detailed; (4) the stamp-book (In kan chio), in this the “stamp”* was contained; (5) the salary-book (Ofuchi chio), showing all that related to salary rice; (6) the rice-purchase book (Kome kaichio); (7) the rice-sale book (Kome uri chio); (8) the receipt-book (Uketori kayoicho), and (9) the sign-book (Otegata chio), in which to make entry of receipts as they came in. Beginning about the year 1724 ad, toward the end of the Tokugawa dynasty, this business developed into something like a banking system, and it lasted till the new regime in 1873, when salaries became payable in currency. The wealth of the bankers and the poverty of their customers gave rise to enactments to help the weaker party. Among these was the compulsory surrender of the right for interest and an allowance of the payment of the money due in installments. The maximum rate of interest on loans was fixed in 1724 at fifteen per cent., in 1743 at twenty per cent., in 1745 at eighteen per cent., in 1788 at twelve per cent., and in 1842 at ten per cent.

BLIND MEN AS LENDERS.

In 1765 ad, a law was passed prohibiting blind men from lending money at usurious rates. It was a custom then for blind men to lend out the funds intrusted to them, and when not paid back, they assembled at the debtor’s Edition: current; Page: [412] house, crying aloud night and day till the money was paid, with a premium in the form of Reikin (gratitude money). In 1832, the legal rate was fixed at twelve per cent., and anything above that rate was to be uncollectible. In 1858, blind men were absolutely prohibited from lending money. These laws were evaded, and the actual rate rose as high as sixty per cent., in addition to various exactions under the name of fees or gratitude moneys. So, in 1871, the usury law was abolished and the matter was left entirely to mutual agreement, and the rate, if not specially defined by contract, was, by the law of 1873, fixed at six per cent. But in 1877 the usury law was re-enacted, though its evasion is as common as before. According to this act, the interest is divided into the court and the market rate. The former is six per cent. and the latter twenty per cent. for sums below 100 yen, fifteen per cent. below 1000 yen, and twelve per cent. for upward of 1000 yen. From what has been said, it must be clear that a proper organization of the money market hardly existed. The high rate of interest was caused not only by the lack of credit on the part of the borrowers, but also by the non-existence of instrumentalities to collect and advance loanable capital. The only recourse open to debtors was to borrow the money of the rich merchants, blind men, and pawnbrokers at usurious rates.

THE GERMS OF REAL BANKING.

Osaka being the commercial centre, and affairs being conducted there on more or less business-like methods, we find that it had the germs of banking long before the adoption of Western institutions. Especially among money-dealers, exchange houses, and contractors to Daimios, branches of the banking business were conducted in a comparatively comprehensive way. To begin with the system of bill brokerage, we find as far back as the middle of the seventeenth century an Osaka merchant, Tennojiya Gorobei, making use of commercial bills. His example was followed by Kohash Jotoko and Kagiya Rokubei; and among these three money-changers bills circulated freely. In 1660 ad, the Inspector-General, Ishimaru, made a code of rules to govern tradesmen, encouraged the growth of credit among them, and established wholesale houses and the Gold Exchange. The number of money-changers was limited to a guild of ten, who transacted a banking business. These ten were allowed to wear swords, a privilege restricted to the class of Samurai; and under them were twenty-two smaller guilds. Among these guilds, with the ten privileged ones as the centre, bills circulated freely. The kinds of bills were seven in all, which may be thus enumerated:

1. Bills of remittance, which were used mostly between the two capitals, the drawer being the Osaka firms and the drawee those in Yedo (now Tokio).

2. Deposit bills, which were issued by the bankers against their depositor, to be paid to him or his order. In this case, if the drawer failed, the loss came on the last holder, the intermediate person or persons being clear of any liability.

Edition: current; Page: [413]3. Bills of exchange, drawn against the exchange houses by their customers or by other houses. If no previous deposit had been made by the drawer, payment was usually refused; but if the exchange house trusted the drawer, the bill was paid up to a certain amount fixed beforehand. When left unpaid, the demand for payment went back to the drawer. If, in spite of the money being deposited by the drawer, the bill was left unpaid by reason of the failure of the exchange house, the loss was borne by the last holder. If demanded on the day assigned and not paid, the drawer was held responsible, but if presented after date, the holder was responsible.

4. Mutual bills (Furisashi gami), which were current among exchange houses only, being issued simply against or with the name of the manager, only the stamp of the drawing houses being affixed. These were settled by 12 m. every day, and even when they were held by an ordinary person, were not payable except at the drawing house.

5. Large bills (Otegata), a name given to bills drawn by large firms on the settling days. For instance, if A, having money to be paid by B, owes to C, A draws a bill against the exchange house and hands it to C. If C hands this bill to his exchange house it is placed to his credit. In the first two days of the following month A gets the money from B and pays it into his exchange house. On the third day, the exchange houses settle the account. In case the bill drawn by A is unpaid, the demand goes back until it reaches the drawer, but the exchange houses never bear the loss.

6. Promissory notes, issued, for instance, by a buyer of goods against an exchange house and handed to the seller, who presents them to the house before the date, in order to ask whether it will be paid when due.

7. Storehouse bills issued against goods, mostly rice and sugar, deposited in storehouses, for ten to thirty days; some, however, remained in store as long as three years, and the bill was highly valued, because if by accident the goods in store were lost or damaged, others were put in their place.

The use of these bills gradually increased by the expansion of trade, chiefly owing to the special protection given them by the law. The suits concerning them were treated as exceptional cases (Naka nuki Saiban), being tried and decided regardless of ordinary court days. When complaints were made, decision was given at once, and if the fault lay with the exchange houses, they were visited with the penalty of handcuffs and imprisonment. The organization of the exchange houses was as nearly as possible perfect. The ten large ones were called the “parent house” (Oya rio gaye), and around them were middle and smaller houses, the smallest being sustained by the next larger till the central house was reached. Usually, against the smaller ones was fixed a limit of credit allowance; and against these credits, bonds or securities, personal and other, were pledged. However, the bill really rested on credit, not much stress being laid on securities. In point of fact, bills were issued far beyond the capacity of these houses; and when they could not pay, the bill was passed on from one holder to the other till it reached and was settled at the parent house. Not only these houses, but Edition: current; Page: [414] every tradesman made use of the bills. Peddlers who came from distant localities gladly received them and the issue rose to an enormous amount, some houses emitting as much as seven-fold the amount of their capital. But as they were payable in chiogin tiogin, or plated coin silver, when this currency was abolished,* in 1868, many houses were unable to pay the bills and became bankrupt, only those whose issue had been kept within moderate limits escaping this fate.

SECTION II.: THE PRESENT.

INSTITUTION OF BANKING PROPER.

THE use of the bills just mentioned being limited mostly to Osaka merchants and the various contractors of each Daimio, belonging, also, for the most part, to one locality, the new era which opened with 1868 made more evident the want of a proper banking system. The Government established Tsushioshi (the Board of Trade) and induced rich merchants to set up companies for trading and bill discounting. Since 1869, discount companies (Kawnase Kaisha) had arisen in Tokio, Yokohama, Nügata, Kioto, Osaka, Kobé, Otsu, and Tsuruga. They were under the control of the Board of Trade, and Government paper notes were given to them as a subsidy, and at the same time to give a currency to this paper, which had been discredited, unpopular, and depreciated. Funds were also placed at their disposal, and they were granted the privilege of issuing gold, silver, dollar, and coin certificates. Of these, silver certificates were issued by the Tokio company and those for coin at Osaka and Kioto, in order to remedy the scarcity of fractional currency. But as they were issued with Government paper notes as the basis, they were, in fact, inconvertible. After a year’s circulation, however, they were supplemented by the small paper money issued by the Government, and by the copper coins which gradually appeared in the market. Except in the case of one-yen notes, all gold certificates were convertible; with the silver certificates we shall deal later. A purely artificial creation of the Government, and managed in a way by no means business-like, in nine cases out of ten, these companies failed. When the National Bank Act came into force in 1872, they had no other alternative but to abide by that law or to submit to the process of liquidation. Most of them showed an enormous total of liabilities and losses. The Government, being their originator, was primarily responsible for them. It recognized this by not only giving up its claims for moneys lent, but by freely advancing funds enough to satisfy the claimants against them. Only the Yokohama Edition: current; Page: [416] company was able to transform itself into a national bank, the other eight being all closed. The dissolution was a matter replete with confusion and difficulty. The notes issued by them, to the amount shown below, were found hard to collect, and their affairs were not quite settled till 1876.

| NAME. | Date of Examination. | Certificate. | Amount. Yen. |

| Tokio Company | 1873 | Gold and Silver. | 2,034,210 |

| Osaka Company | 1873 | Coin. | 1,408,034.2 |

| Gold. | 1,853,450 | ||

| Yokohama Company | 1873 | Gold. | 1,500,000 |

| Kioto Company | 1873 | Coin. | 1,276,313.450 |

| Gold. | 640,000 | ||

| Otsu Company | 1873 | Gold. | 262,500 |

| Kobé Company | 1873 | Gold. | 500,000 |

| Nügata Company | 1874 | Gold. | 50,000 |

| Tsuruga Company | 1873 | Gold. | 41,000 |

These failures taught the Government a hard but a salutary lesson. It became henceforth more careful and deliberate in encouraging the rise of companies. Though schemes for banks and other companies were submitted in various parts of the country, they were not readily approved. It was expressly stated in one of the clauses of the Bank Act that: “Those who desire to transact exchange, bill discount, deposit, loan and any other business closely related to banking, must hereafter obtain the permission of the Comptroller of the Currency before they commence business. Banks or companies who are already in business must present reports to the Treasury according to the prescribed form.”

GOVERNMENT SUPERVISION.

As the result of this enactment, the control of these “quasi-banks,” which was in the hands of the Bureau of General Affairs, was transferred to the office of the Comptroller of the Currency. There were many cases, however, in which the Government charter was abused by speculators for the purpose of acquiring funds to be devoted to their own use. Many concerns called themselves banks without any legal recognition. The public could not distinguish the regular from the irregular, and general distrust began to prevail. So, in 1872, a notification was issued by the Treasury prohibiting the use of the word “bank,” except by those having the permission of the Treasury. As there was no special law governing these institutions, the grant was given in most cases where no harm was expected to follow. But there were many who used the grant for fraudulent purposes, and not a few surrendered the right even before they did any business. The loss entailed on the public was considerable. An order leaving the provision of proper Edition: current; Page: [417] banking safeguards to mutual agreement was promulgated in 1874. Much inconvenience and confusion resulted. A proposal to formulate a banking law was discussed, but was set aside on the ground that such a measure was premature, since even a general commercial code did not exist. In 1878, the power to permit the organization of banks was delegated to the prefect of each locality. This gave rise to locally divergent practice; in some places the grant being given freely, while in others very strict requirements were insisted on. So, in 1882, an order was issued commanding prefects to ask the opinion of the Treasury before reaching a decision, and to present to the department a draft of the by-laws and regulations of the banks. Also in this year, the quasi-banks were authoritatively defined to be those which make loans, receive deposits, or discount bills. There had thus come into existence the following varieties of banks:

1. Those established with the Government permission. Among these there were two kinds; namely, those having the permission of the Treasury and those directly authorized by the prefect.

2. Those left entirely to the regulation of a mutual contract.

3. Those established without any governmental recognition.

Between these three no clear distinction whatever was made, and they were all equal in the eye of the law. However, there were some limitations, such as:

1. The liability of shareholders was held to be unlimited; this restriction was, however, removed and limited liability recognized, in 1886, for banks whose capital stock exceeded 500,000 yen.

2. The capital must not be less than 10,000 yen.

3. The capital must be paid up at least within a year.

4. The dealing in stocks, shares, and merchandise, which did not properly belong to the banking business, was prohibited.

The receipt of savings, which was allowed till 1884 to ordinary banks, was also prohibited, as was the opening of savings-banks. In 1886, an order was issued commanding banks to report to the Treasury. But in 1890, the commercial code was promulgated, as also the laws concerning banks and savings-banks. It was provided that the whole system should come into simultaneous operation in the beginning of 1891, but by resolution of the Diet, the date was postponed till July 1, 1893. The main features of the banking law will be best understood by a reference to its text.

THE BANK ACT OF 1890.

Art. I. If any person, corporate or individual, discount negotiable bills, transact exchange, or receive deposits and advance loans at the same time, as a profession, in an open shop, he or it becomes a bank whether so designated or not.

Art. II. Those who want to do a banking business must fix the amount Edition: current; Page: [418] of the capital to be employed, and permission of the Secretary of the Treasury must be obtained through the interposition of the prefect.

Art. III. Banks must present half-yearly reports to the Treasury, through the hands of the prefect.

Art. IV. Banks must make public every half-year, a list of assets and a balance-sheet, in the columns of a newspaper or by some other method of advertising.

Art. V. Banks must not advance as loans or on discount any sum beyond one-tenth of their capital to one customer. Those whose capital is not wholly paid up must not use more than one-tenth of the paid-up capital.

Art. VI. The business hours of the banks are to be between 10 a. m. and 4 p. m., though they may be prolonged at the convenience of the bank.

Art. VII. Banks may be closed on national holidays and feast days, Sundays, and other resting days, according to the custom of each locality. If they desire to close outside of those days, they can do so after notifying the prefect and advertising the fact in newspapers or by other means.

Art. VIII. The Minister of Finance can order the inspection of banks by the prefect or any other officials.

Art. IX. If in violation of article two, banking business is done without due permission, the offender is to be punished according to article 256* of the Commercial Code.

Art. X. If banks neglect to present the report prescribed in article three or to publish their accounts in pursuance of article four, or if they make fraudulent statements or conceal the truth, the penalty fixed in article 262† of the Commercial Code will be imposed. If the inspection ordered in article eight be refused, article 258‡ of the code is to apply.

Art. XI. This act does not apply to the Bank of Japan, the Yokohama Specie Bank, or the national banks.

THE SAVINGS-BANK ACT.

Art. I. Those in receipt of savings as deposits are savings-banks. If any bank receive a deposit, whether casual or fixed, which is less than five yen at a time, it will be considered as a savings-bank and must be subject to this act.

Art. II. The savings-bank must be a joint-stock company of not less than 30,000 yen capital.

Art. III. The directors of savings-banks must be subject to unlimited liability, which lasts for a year at least.

Art. IV. Savings-banks must deposit a sum not less than one-half of the Edition: current; Page: [419] paid-up capital in interest-bearing Government bonds as a guarantee for deposits.

Art. V. Savings-banks must not transact any business except in (1) loans; (2) discounting of negotiable instruments; (3) purchase of national or local debt bonds.

Art. VI. When money is to be advanced on loan, the term must be within six months, with national or local debt bonds as securities. In case of discount, it is restricted to bills of exchange and promissory notes, with at least two trustworthy indorsers. Savings-banks cannot buy and sell national or local debt bonds as part of their regular business.

Art. VII. When by-laws are to be modified, the permission of the Minister of Finance must be obtained through the intervention of the prefect.

Art. VIII. Banks desiring to do the business of a savings-bank must obtain authorization from the Minister of Finance through the intervention of the prefect.

Art. IX. If savings-banks violate any provision of this act, a penalty of not less than fifty yen and not more than 500 yen is imposed on the directors. A similar penalty attaches to the doing of a savings-bank business without due authorization.

Art. X. Except as to the points specially covered by this act, the regulations of the Bank Act are applicable to savings-banks also.

In accordance with these laws, orders were issued by the Treasury in May, 1893. Prior to this legislation, many important banks were formed—for instance, the Mitsui Bank, which was established in 1873. But at the time when the national bank scheme found general acceptance, about the year 1879, the organization of common banks came almost to a standstill. But since 1880 a sudden increase of these banks has taken place, the fate of a good many of which has been to be wound up or amalgamated, as shown in table on page 420.

Edition: current; Page: [420]| YEAR. | NUMBER. | CAPITAL. | |||||||

| New Institutions. | Closure or Amalgamation. | Total Remain’g | Original Capital. | Added Capital. | Liquidated or Decreased Capital. | Net Remaining Capital. | |||

| YEN. | YEN. | YEN. | YEN. | ||||||

| 1876 | 1 | 1 | 2,000,000,000 | 2,000,000,000 | |||||

| 1877 | |||||||||

| 1878 | |||||||||

| 1879 | 8 | 9 | 1,680,000,000 | 3,680,000,000 | |||||

| 1880 | 29 | 38 | 3,330,000,000 | 7,010,000,000 | |||||

| 1881 | 47 | 85 | 3,607,000,000 | 220,000,000 | 10,837,000,000 | ||||

| 1882 | 80 | C. | 1 | 164 | 5,508,000,000 | 622,000,000 | L. | 30,000,000 | 16,937,000,000 |

| 1883 | 35 | 199 | 1,520,750,000 | 18,457,750,000 | |||||

| 1884 | 20 | { A. | 1 } | 213 | 1,276,300,000 | 270,000,000 | { L. | 750,000,000 } | 19,025,050,000 |

| { C. | 5 } | { D. | 229,000,000 } | ||||||

| 1885 | 14 | C. | 10 | 217 | 550,000,000 | 65,000,000 | { L. | 545,000,000 } | 18,362,200,000 |

| { D. | 732,850,000 } | ||||||||

| 1886 | 11 | C. | 9 | 219 | 1,045,000,000 | 35,000,000 | { L. | 1,030,000,000 } | 17,539,025,000 |

| { D. | 873,175,000 } | ||||||||

| 1887 | 11 | C. | 12 | 218 | 981,000,000 | 847,000,000 | { L. | 653,925,000 } | 18,371,385,500 |

| { D. | 341,714,000 } | ||||||||

| 1888 | 25 | { A. | 2 } | 230 | 1,919,500,000 | 246,000,000 | { L. | 830,360,000 } | 19,216,200,000 |

| { C. | 11 } | { D. | 487,325,000 } | ||||||

| 1889 | 31 | C. | 6 | 255 | 3,145,000,000 | 390,000,000 | { L. | 339,000,000 } | 22,059,975,000 |

| { D. | 355,225,000 } | ||||||||

| 1890 | 24 | C. | 7 | 272 | 3,573,000,000 | 463,000,000 | { L. | 411,700,000 } | 25,571,175,000 |

| { D. | 113,100,000 } | ||||||||

| 1891 | 31 | C. | 9 | 294 | 1,835,000,000 | 403,000,000 | { L. | 365,500,000 } | 27,060,775,000 |

| { D. | 382,900,000 } | ||||||||

| 1892 | 43 | C. | 13 | 324 | 2,532,700,000 | 463,500,000 | { L. | 536,500,000 } | 28,834,775,000 |

| { D. | 685,700,000 } | ||||||||

| Total. | 410 | 86 | 34,503,250,000 | 4,024,500,000 | 9,692,975,000 | ||||

The case of the quasi-banks was not much better, as the following table indicates:

| YEARS. | NUMBER. | CAPITAL. | ||||||

| New Banks. | Transformation or Closure. | Number Remaining. | Original Capital. | Increased Capital. | Liquidation or Decrease. | Net Capital Left. | ||

| YEN. | YEN. | YEN. | YEN. | |||||

| 1884 | 45 | C. | 3 | 741 | 1,092,152,000 | 27,200,000 | D. 20,000,000 | 15,227,685,000 |

| 1885 | 20 | T. | 1 } | 745 | 590,530,000 | 103,909,000 | { L. 270,559,000 } | 15,407,982,000 |

| C. | 15 } | { D.243,583,000 } | ||||||

| 1886 | 24 | C. | 20 } | 749 | 560,950,000 | 59,333,000 | { L. 280,126,000 } | 15,401,304,000 |

| { D.346,835,000 } | ||||||||

| 1887 | 10 | T. | 1 } | 741 | 247,500,000 | 12,000,000 | { L. 387,300,000 } | 15,117,676,000 |

| C. | 17 } | { D. 155,828,000 } | ||||||

| 1888 | 11 | T. | 2 } | 711 | 222,950,000 | { L. 723,345,000 } | 14,408,264,140 | |

| C. | 39 } | { D. 209,016,860 } | ||||||

| 1889 | 15 | T. | 4 } | 695 | 600,000,000 | 54,121,000 | { L. 482,612,000 } | 14,421,003,140 |

| C. | 27 } | { D. 158,770,000 } | ||||||

| 1890 | 18 | T. | 4 } | 702 | 247,000,000 | 122,980,000 | { L. 186,863,000 } | 14,512,616,000 |

| C. | 7 } | { D. 91,504,140 } | ||||||

| 1891 | 13 | T. | 5 } | 678 | 261,758,000 | 63,150,000 | { L. 880,290,000 } | 13,827,434,000 |

| C. | 30 } | { D. 129,800,000 } | ||||||

| 1892 | 14 | T. | 2 } | 680 | 220,000,000 | 137,100,000 | { L. 208,390,000 } | 13,944,644,000 |

| C. | 10 } | { D. 31,500,000 } | ||||||

| Total. | 170 | 187 | 4,042,840,000 | 579,793,000 | 4,816,322,000 | |||

With the enactment of these laws in 1893, many unsound companies gave up business or were dissolved, and the number of common and quasi banks suddenly decreased. At the end of 1893 they stood thus:

| a | Permitted to continue business | 518, | with a capital of | 32,952,216 yen |

| b | Still in quest of a grant | 43, | with a capital of | 1,539,390 yen |

| c | Newly established | 40, | with a capital of | 1,506,890 yen |

| Total | 605, | with a capital of | 35,998,496 yen |

| a | Permitted to continue business | 22, | with a capital of | 1,010,000 yen |

| b | Still in quest of a grant | 2, | with a capital of | 130,000 yen |

| c | Newly established | with a capital of | yen | |

| Total | 24, | with a capital of | 1,140,000 yen |

Since then, many banks have been set up in different parts of the country, and bankers began to complain of the restrictive character of these acts. So, Edition: current; Page: [422] in February, 1895, a law was passed which amended the Bank Act and made it much more liberal, abolishing article five and changing the business hours to between 9 a. m. and 3 p. m. Moreover, in March, the Savings Bank Act was greatly modified. Although the liability of directors was made to last two years instead of one, other amendments were on the side of greater liberality. Articles four, five, and six were thus supplemented:

Art. IV. Savings-banks must deposit a sum of not less than one-fourth of their total deposits in national or local debt bonds as a guarantee for the repayment of depositors. If the guarantee is equal to more than one-half of the capital, they may use commercial bills, loan certificates, or shares of companies of good standing.

Art. V. The amount of the deposit to be calculated, in the above article, is that which remains at the end of each half-year.

Art. VI. Depositors have a preferential claim on the securities deposited according to article four.

This liberal policy stimulated the further establishment of banks and savings-banks. Even those who were merely money-lenders found it better to command the force of a banking corporation. Quasi-banks which had given up the business took it up again. Moreover, the general expansion of commerce increased the necessity for credit institutions. In fact, a mania for establishing banks set in, the result of which is shown in the enormous increase of banks and their capital, as set forth in the following table:

| BANKS. | 1893. | 1894. | 1895. | |||

| Number. | Capital. | Number. | Capital. | Number. | Capital. | |

| YEN. | YEN. | YEN. | ||||

| Joint-stock banks | 486 | 26,558,450 | 584 | 42,083,990 | 666 | 65,855,539 |

| Savings-banks | 24 | 1,140,000 | 34 | 1,470,000 | 89 | 4,553,000 |

| Partnership banks | 15 | 2,912,400 | 17 | 2,977,400 | 19 | 3,037,400 |

| Commandite banks | 44 | 3,793,620 | 58 | 5,058,090 | 71 | 6,764,230 |

| Private banks | 59 | 2,724,020 | 69 | 2,658,420 | 68 | 3,955,520 |

| Total | 628 | 37,128,490 | 761 | 54,277,900 | 913 | 84,165,689 |

TENDENCY TOWARD CONSOLIDATION.

The fact that there are too many banks, and that some of them have too limited a capital and have a dubious chance of success, is not calculated to cause sanguine expectations of the future. However, by the operation of the law of the survival of the fittest, the soundest will remain. This is an optimistic view. But there are influential men who begin to be impressed with the necessity of consolidating small banks by way of putting an end to the demoralizing kind of competition among them. Amalgamation, Edition: current; Page: [423] according to the commercial code, is impossible, except one bank is dissolved and the other has an increase of capital, or both are dissolved and a new one is established in their place. In any case, the trouble involved in the process makes it hardly possible to expect that amalgamation will be extensively carried out. If by a special law it were made possible for one to join another without the tedious and complex work of winding up, so long as the absorbing bank assumes the rights and duties of the one absorbed, the hope might be more easy of fulfillment. In this direction nothing can be done unless capital be concentrated and banks made more powerful. Such is the work to be accomplished by bankers, aided by the legislature in the future, and, though the task is by no means an easy one, there can be no question about its imperative necessity. In order to show the volume of ordinary banking transactions for the seven years 1888-94, the following table is inserted:

| YEARS. | Cash Receipts & Payments. | DEPOSITS. | Loans. | DRAFTS. | Bills on Goods. | Bills Discounted. | Bills for Collect’n. | ||

| Public. | Private. | Public. | Private. | ||||||

| YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | |

| 1888 | 1,535,379,694 | 5,529,442 | 14,527,993 | 28,697,174 | 31,058,039 | 71,077,373 | 8,277,989 | 23,705,458 | 7,187,856 |

| 1889 | 1,013,962,549 | 6,615,947 | 18,288,497 | 36,698,170 | 27,803,970 | 88,777,821 | 8,333,704 | 17,237,566 | 6,311,861 |

| 1890 | 1,973,090,027 | 4,502,727 | 20,836,251 | 39,537,835 | 28,912,215 | 104,518,759 | 9,817,240 | 36,335,987 | 9,990,907 |

| 1891 | 2,008,719,524 | 3,242,972 | 21,450,523 | 40,922,441 | 22,508,462 | 97,875,387 | 11,284,638 | 42,148,241 | 8,048,361 |

| 1892 | 2,201,820,981 | 4,864,467 | 27,659,515 | 33,736,165 | 22,036,779 | 100,887,704 | 13,904,584 | 54,805,903 | 7,809,930 |

| 1893 | 1,685,216,008 | 2,807,568 | 35,618,642 | 50,149,802 | 28,259,236 | 87,628,334 | 24,241,741 | 38,121,069 | 6,945,359 |

| 1894 | 3,794,748,889 | 63,246,082 | 504,173,882 | 254,850,278 | 64,094,127 | 193,483,485 | 40,536,780 | 102,613,991 | 16,055,346 |

| [NOTE.—The new Bank Act came into force in July, 1893, and the figures for 1893 are those of the half-year ending in December.] | |||||||||

Such being the state of things, many who entertain pessimistic views complain of the want of activity and capacity among our banks, deeming them, as a rule, nothing better than pawnbrokers and usurers who make a profit by lending out at a higher rate of interest than that at which they borrow from the larger banks, such as the Bank of Japan and national banks. Some also fear the coming of a crisis, because of excessive competition and profuse allowance of credit on the part of the banks. But as the law now stands, it is impossible to limit their number or to regulate the details of their management. So, the matter must be left to the discretion and prudence of the public. Much, however, can be and is being done in the way of correction by the Government inspection and publication of bank accounts. As for those organized hereafter, investigation and precaution on the part of the prefect may prevent the consummation of unsound undertakings. As an offset against the bad cases, the increase of banks by lowering the rate of interest tends to benefit the country, which seems to be in need of institutions of credit.

CHAPTER II.: THE NATIONAL BANKS.

SECTION I.: THEIR ORIGIN AND ORGANIZATION.

THE OLD BANK ACT.

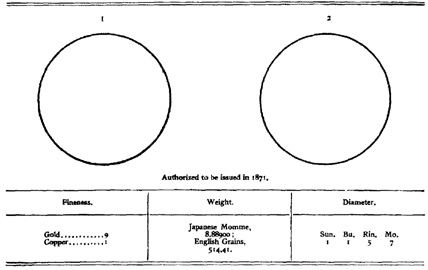

AT the beginning of the new era (Meiji), the lack of an organized banking system was keenly felt by the people and by the Government, which suffered greatly from the confused state of its depreciated paper currency. In 1870, the Vice-Minister of Finance, Mr. Ito (now Marquis) went to the United States of America to investigate the banking system of that country. One result of this visit was his advice to adopt the system of national banks which he found there. Though some approved of the recommendation, many opposed it on the ground that the system was risky and unsuited to the needs of the country. Its opponents upheld the principle of a full gold reserve, and though the subject was hotly discussed, no practical result was reached. In 1871, a scheme of setting up a bank of issue with 7,000,000 yen capital was considered by the Tokio Chamber of Commerce. But the difficulty of getting the necessary funds frustrated the scheme. On his return in the same year, Mr. Ito urged the necessity and advantage of the American system, and his views were finally adopted. Out of this decision, in November, 1872, came the National Bank Act, being No. 349 of the laws of that year. This law is what is now designated as the old National Bank Act. Under it, banks were allowed to issue notes convertible in gold, holding Government bonds issued for the redemption of Government paper notes as the basis, to sixty per cent. of the capital, which was not to be less than 50,000 yen. This may be described as a compromise between Edition: current; Page: [425] the American and the gold reserve systems, fulfilling at the same time the purpose of redeeming the Government paper notes with the bond, and with this bond as the basis of banking, issuing convertible notes, which were to be finally converted into gold when the time for redemption of these bonds arrived. However, contrary to expectation, this many-sided and ingenious scheme ended in utter failure, and but four banks were formed under the act. Only 1,420,000 yen of bank notes were actually received by them, out of 15,000,000 yen which were printed in New York beforehand. The cause of this failure was the depreciation of paper notes in general, on account of the constant efflux of bullion due to the importation of goods and the over-issue of Government notes, as well as to the fact of the bank notes being immediately convertible into gold.* This latter facility operated so that the Second National Bank, located in Yokohama, the chief commercial port, could not issue even one yen of its notes. Consequently, the amount of bank notes in actual circulation, which stood at 1,356,979 yen in June, 1874, made a rapid descent to 62,456 yen in 1876, regardless of the exertions of the Government to keep up the volume of the circulation. With such a limited amount of currency and a very slender total of deposits, the only source of profit for the banks was the interest of six per cent., accruing from the Government bonds, while the market rate of interest was above ten per cent. The four existing banks presented a petition to the Government in March, 1875, to allow their notes to be convertible into Government notes only. This being equivalent to a return to the former state of non-convertibility, the Government hesitated, but in order to give relief to the petitioners, the Government issued its notes, which were inconvertible, to the amount of one-half of the issue of the Bank, a corresponding amount of bank notes being paid into the Exchequer. In 1876, the depreciation of paper money went from bad to worse† and the difficulty still increasing, the banks again petitioned the Government to exchange the remaining half of their notes for Government paper money. To this the Government acceded, and the scheme, so full of promise, fell through.

THE REVISION OF THE ACT.

It became clear that the result of the over-issue of the Government notes could not be corrected through the national banks, and still more clear that under such a banking system the need of the time could not be supplied. The necessity of revising the Bank Act was therefore demonstrated. There was one more important reason for the revision; and to explain this, we must go back to the issue of a Government loan to the amount of more than 174,000,000 yen to pay off feudal pensioners who gave up their hereditary rights in exchange for Government bonds.‡ How to keep up the price of Edition: current; Page: [426] these bonds, for the benefit of their owners, was a problem which the kind-hearted policy of the Government of that time recognized. An idea entered the head of Count Okuma, the Minister of Finance, which was embodied in the Revised National Bank Act, promulgated by Law No. 106, in August, 1876. According to this act, bank notes of 1, 2, 5, 10, 20, 50, 100, and 500 yen denominations being legal tender except for the payment of customs duty and interest on Government bonds, became convertible into Government paper money instead of into standard gold, and the newly issued pension bonds were used as a basis for these notes. Besides, the amount of the bonds to be deposited in the Treasury by the banks was increased from sixty to eighty per cent. of the capital, and the kind of bonds was made optional so long as it bore four per cent. interest. The most important change consisted in a gold reserve of forty per cent. of the capital (⅔ of the issue) being transformed into a paper money reserve of twenty per cent. of the capital (¼ of the issue). Thus the American system was at last adopted nearly in its entirety. The idea of metallic conversion was given up, and the fall in price of the bonds was somewhat retarded, the owners of the bonds becoming shareholders of national banks to the extent of seventy per cent. of the whole. This radical change made the banking business remunerative, and many new national banks sprung up, five being organized during 1876, twenty-three in 1877, ninety-eight in 1878, and twenty-seven in 1879, making, in all, 153.

THE FINAL REVISION OF THE ACT.

The organization of banks became so prevalent that in December, 1877, by Law No. 83, the Bank Act was amended, empowering the Minister of Finance to restrict, on the basis of population and taxation, the total amount of the issue of bank notes, which was fixed at 40,000,000 yen, as well as the number and capital of the national banks. Though this law was supplemented by a subsequent act, Law No. 5, of 1878, the main features remained the same. With the increase of note circulation, the depreciation of paper, the rise of prices, and the fall in value of Government bonds became more emphatic. In order to remedy these evils, especially to unify the paper currency, the Nippon Ginko (the Bank of Japan) was established in 1882, and a radical revision of the National Bank Act was carried out in 1883 by Law No. 14. The main points of the revision were:

1. The national banks are to cease to have the privilege of issuing notes at the expiration of their term of existence, which is to be after twenty years from the date of their obtaining their charter. After the end of the term they may continue to conduct the banking business simply and solely as a common bank, with the permission of the Secretary of the Treasury.

2. They must redeem their notes within their term of existence as national banks. In order to fulfill this obligation, they must create a fund consisting of the reserve (twenty per cent. of capital) already held by the banks Edition: current; Page: [427] and the annual reserve out of the profits to the amount of two and a half per cent. of the originally prescribed limit for the issue of paper notes. This fund is to be intrusted to the Bank of Japan, which is to purchase Government stocks, and with the accruing interest to redeem bank notes twice a year.

THE RISE AND FALL.

After the close of the civil war of 1877, the general rise of prices created a brisk state of trade, which reached its climax in 1880 and 1881. But in the latter year, Count Matsukata was placed in control of the Treasury, and his policy was to put the finances of the country on a firm and solid basis. The redemption of paper money was begun, prices and interest fell, trade seemed to be depressed, and many failures ensued. Even first-rate national banks had to take measures of precaution, the weaker ones had to lessen their capital to make good their losses; four national banks became bankrupt, five others being temporarily suspended during a short interval between 1882 and 1883, and ten banks being consolidated with more powerful banks between 1880 and 1885. But in 1886 redemption in specie commenced, and things became more settled, trade began to revive, and railway and other companies sprang into existence. In 1887, trade became active again, speculation in stocks grew apace, and many national banks increased their capital. Since then, nothing remarkable has taken place except a few failures, suspensions, and amalgamations.

RESTRICTIVE REGULATIONS.

The dividends of national banks are usually greater than those of other banks, because they reap a double benefit by lending out their notes and obtaining the interest on the bonds deposited as security for those notes in the Treasury. Against these special privileges and advantages, they are under the strict surveillance of law and Government control, and are subject to many other restrictions. First of all, they must pay the bank tax fixed at seven-tenths of one per cent. of the original note issue; their functions are restricted to making loans, receiving deposits, making transfers of money, and discounting bills. Though they can sell and purchase Government bonds, foreign coin, and bullion, as well as exchange coins, these cannot be made their chief business. Transactions in land, buildings, or other property, as well as in shares of joint-stock companies, are prohibited to them, except the property be for their own use, or in case of its falling temporarily into their hands on pledge or mortgage. Though the restriction on the rate of interest, which was fixed at ten per cent. in the Act of 1876, was removed, they have to conform to the Usury Act, and they cannot lend to one customer more than ten per cent. of their capital. Neither against bank notes nor their own stock can they make loans, and of their total deposits they must keep in hand twenty-five per cent. in order to meet a sudden demand. Except Edition: current; Page: [428] on regular holidays, the office must be opened from 9 a. m. to 3 p. m.; a general meeting of stockholders must be held twice a year; and for all important resolutions, Government recognition must be obtained, and monthly as well as half-yearly reports must be submitted to the Treasury. Above all, it is prohibited to national banks to enter into correspondence with foreign banks in or out of the country, or even with banks organized by Japanese citizens and located abroad, without permission of the Treasury. Permission must be requested beforehand for the payment of dividends, for the increase or decrease of capital, for changes in the by-laws of the bank, or for voluntary dissolution. Any speculative undertaking by the banking staff is strictly forbidden, as well as their borrowing from the bank beyond the sum fixed in the by-laws. The control of national banks is vested in the Third Bureau of the Treasury, which sends out its own officials at stated times to examine the actual working of the banks, and which sometimes delegates the power of inspection to the local prefect. The Secretary of the Treasury has the power to suspend the business of a bank in any of the following cases, and he can further order the dissolution of the bank:

- 1. Violation of the letter or spirit of the Bank Act.

- 2. Discovery of evidence that the bank cannot pay its debts.

- 3. A series of loans in excess of the capital.

In the case alike of voluntary winding up and official dissolution, the obligation to redeem the outstanding notes falls on the Government. This is met by selling the Government bonds invested in by the bank, and paying note-holders within a date fixed by departmental notice. These general provisions affect equally all the 133 national banks which now exist, though there are, of course, great differences in their actual working, and in the degree of public confidence which they possess.

THE EXISTING CONDITION.

The present state of the national banks may best be seen in the following tables, pages 429-435.

Edition: current; Page: [429]| Number. | No. of Branch Offices. | Date of Charter. | Expiration. | Capital. | Original Issue of Notes. | Present Amount of Issue. | Government Bonds as Basis. | AMOUNT OF THE REDEMPTION FUND. | ||

| Reserve Fund. | Accumulation Fund. | Total. | ||||||||

| YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | ||||

| 1 | 11 | Sept., 1876. | Sept., 1896. | 2,250,000 | 1,200,000,000 | 182,753,500 | 807,552,000 | 377,842,520 | 366,201,810 | 744,044,330 |

| 2 | 4 | Nov., 1876. | Nov., 1896. | 500,000 | 400,000,000 | 78,450,000 | 305,568,000 | 125,947,501 | 122,067,266 | 248,014,767 |

| 3 | 4 | Dec., 1876. | Nov., 1896. | 1,000,000 | 800,000,000 | 615,156,000 | 538,440,000 | 251,895,011 | 244,134,538 | 496,029,549 |

| 4 | 2 | Dec., 1876. | Dec., 1896. | 500,000 | 240,000,000 | 43,046,500 | 168,960,000 | 75,568,500 | 73,240,359 | 148,808,859 |

| 5 | 2 | Oct., 1876. | Oct., 1896. | 300,000 | 240,000,000 | 44,664,500 | 161,760,000 | 75,568,500 | 73,240,359 | 148,808,859 |

| 6 | 2 | Feb., 1877. | Feb., 1897. | 250,000 | 200,000,000 | 123,518,500 | 138,240,000 | 62,973,749 | 61,033,630 | 124,007,379 |

| 7 | Feb., 1877. | Feb., 1897. | 150,000 | 112,000,000 | 45,977,000 | 78,816,000 | 35,265,297 | 34,178,830 | 69,444,127 | |

| 8 { | Feb., 1877. | { Amalgamated with No. 134 in 1886. } | ||||||||

| 9 | 2 | Nov., 1877. | Nov., 1897. | 250,000 | 80,000,000 | 48,194,000 | 56,400,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 10 | 2 | Mar., 1877. | Mar., 1897. | 250,000 | 200,000,000 | 100,478,000 | 141,120,000 | 62,973,749 | 61,033,630 | 124,007,379 |

| 11 | May, 1877. | May, 1897. | 200,000 | 160,000,000 | 89,083,500 | 125,760,000 | 50,378,997 | 48,826,900 | 99,205,897 | |

| 12 | 9 | July, 1877. | July, 1897. | 500,000 | 224,000,000 | 95,060,500 | 152,806,250 | 70,530,602 | 68,357,666 | 138,888,268 |

| 13 | 2 | May, 1877. | May, 1897. | 500,000 | 400,000,000 | 225,266,000 | 269,280,000 | 125,947,501 | 122,067,266 | 248,014,767 |

| 14 | July, 1877. | July, 1897. | 150,000 | 80,000,000 | 17,395,000 | 53,856,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 15 | May, 1877. | May, 1897. | 17,826,100 | 14,260,880,000 | 8,313,747,500 | 9,600,000,000 | 4,490,305,728 | 4,351,966,779 | 8,842,272,509 | |

| 16 | Aug., 1877. | Aug., 1897. | 200,000 | 80,000,000 | 45,372,500 | 56,352,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 17 | 2 | Sept., 1877. | Sept., 1897. | 300,000 | 160,000,000 | 93,094,500 | 107,688,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 18 | 3 | Nov., 1877. | Nov., 1897. | 500,000 | 200,000,000 | 101,397,000 | 138,048,000 | 62,973,749 | 61,033,630 | 124,007,379 |

| 19 | 2 | Oct., 1877. | Oct., 1897. | 200,000 | 120,000,000 | 54,657,000 | 81,120,000 | 37,784,249 | 36,620,177 | 74,404,426 |

| 20 | 3 | July, 1877. | July, 1897. | 250,000 | 200,000,000 | 49,279,000 | 140,736,000 | 62,973,749 | 61,033,630 | 124,007,379 |

| 21 | Nov., 1877. | Nov., 1897. | 100,000 | 80,000,000 | 19,023,500 | 57,072,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 22 | 2 | Oct., 1877. | Oct., 1897. | 300,000 | 232,000,000 | 185,586,000 | 163,248,000 | 73,049,547 | 70,799,011 | 143,848,558 |

| 23 | 2 | Oct., 1877. | Oct., 1897. | 200,000 | 144,000,000 | 104,251,000 | 101,424,000 | 45,341,098 | 43,944,213 | 89,285,311 |

| 24 | Oct., 1877. | Closed in 1882. | ||||||||

| 25 | 1 | Dec., 1877. | Dec., 1897. | 130,000 | 104,000,000 | 88,147,500 | 73,920,000 | 32,746,347 | 31,737,487 | 64,483,834 |

| 26 | Feb., 1878. | Closed in 1883. | ||||||||

| 27 | Dec., 1877. | Dec., 1897. | 300,000 | 200,000,000 | 157,647,000 | 140,688,000 | 62,973,749 | 61,033,630 | 124,007,379 | |

| 28 { | Dec., 1877. | { Amalgamated with No. 35 in 1889. } | ||||||||

| 29 | 2 | Jan., 1878. | Jan., 1898. | 200,000 | 80,000,000 | 72,961,000 | 56,640,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 30 | Dec., 1877. | Dec., 1897. | 350,000 | 280,000,000 | 230,145,000 | 211,200,000 | 88,163,250 | 85,447,084 | 173,610,334 | |

| 31 { | Mar., 1878. | { Amalgamated with No. 148 in 1888. } | ||||||||

| 32 | 2 | Jan., 1878. | Jan., 1898. | 360,000 | 288,000,000 | 254,127,500 | 198,720,000 | 90,682,201 | 87,888,429 | 178,570,630 |

| 33 | Jan., 1878. | Closed in 1892. | ||||||||

| 34 | 2 | Mar., 1878. | Mar., 1898. | 375,000 | 200,000,000 | 182,376,500 | 143,040,000 | 62,973,749 | 61,033,630 | 124,007,379 |

| 35 | 5 | May, 1878. | May, 1898. | 600,000 | 312,000,000 | 269,542,500 | 210,240,000 | 98,239,044 | 95,212,462 | 193,351,506 |

| 36 | Feb., 1878. | Feb., 1898. | 200,000 | 80,000,000 | 72,997,000 | 56,640,000 | 25,189,497 | 24,413,447 | 49,602,945 | |

| 37 | 1 | Oct., 1878. | Oct., 1898. | 250,000 | 120,000,000 | 109,168,000 | 90,480,000 | 37,784,249 | 36,620,177 | 74,404,426 |

| 38 | 1 | Oct., 1878. | Oct., 1898. | 400,000 | 184,000,000 | 169,327,500 | 127,248,000 | 57,935,849 | 56,150,938 | 114,086,787 |

| 39 | 1 | Sept., 1878. | Sept., 1898. | 700,000 | 280,000,000 | 254,960,000 | 188,448,000 | 88,163,250 | 85,447,084 | 173,610,334 |

| 40 | 4 | Sept., 1878. | Sept., 1898. | 560,000 | 120,000,000 | 109,355,000 | 84,624,000 | 37,784,249 | 36,620,177 | 74,404,626 |

| 41 | 2 | Sept., 1878. | Sept., 1898. | 300,000 | 160,000,000 | 145,439,500 | 112,800,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 42 | Oct., 1878. | Oct., 1898. | 250,000 | 200,000,000 | 181,968,000 | 137,808,000 | 62,973,749 | 61,033,630 | 124,007,379 | |

| 43 | 3 | Oct., 1878. | Oct., 1898. | 300,000 | 160,000,000 | 145,995,000 | 110,400,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 44 { | July, 1878. | { Amalgamated with No. 3 in 1882. } | ||||||||

| 45 | Oct., 1878. | Oct., 1898. | 200,000 | 120,000,000 | 109,280,000 | 83,040,000 | 37,784,247 | 36,620,175 | 74,404,422 | |

| 46 | Feb., 1879. | Feb., 1899. | 150,000 | 40,000,000 | 36,411,000 | 30,384,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 47 | 3 | Oct., 1878. | Oct., 1898. | 150,000 | 76,000,000 | 69,221,500 | 51,168,000 | 23,930,022 | 23,192,773 | 47,122,795 |

| 48 | Dec., 1878. | Dec., 1898. | 100,000 | 80,000,000 | 72,608,500 | 53,856,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 49 | May, 1878. | May, 1898. | 400,000 | 160,000,000 | 145,702,000 | 115,296,000 | 50,378,997 | 48,826,900 | 99,205,897 | |

| 50 | Aug., 1878. | Aug., 1898. | 135,000 | 80,000,000 | 72,863,500 | 53,856,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 51 | Sept., 1878. | Sept., 1898. | 100,000 | 80,000,000 | 72,910,000 | 56,352,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 52 | 1 | Sept., 1878. | Sept., 1898. | 150,000 | 80,000,000 | 73,006,000 | 57,120,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 53 | 3 | Dec., 1878. | Dec., 1898. | 120,000 | 64,000,000 | 58,213,500 | 45,120,000 | 20,151,596 | 19,330,756 | 39,682,332 |

| 54 { | Sept., 1878. | { Amalgamated with No. 35 in 1882. } | ||||||||

| 55 | Sept., 1878. | Dec., 1898. | 50,000 | 40,000,000 | 36,311,000 | 28,512,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 56 | 1 | June, 1878. | June, 1898. | 150,000 | 64,000,000 | 58,307,500 | 45,059,250 | 20,151,596 | 19,530,756 | 39,682,352 |

| 57 | Oct., 1878. | Oct., 1898. | 50,000 | 40,000,000 | 36,947,000 | 27,840,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 58 | 3 | Oct., 1878. | Oct., 1898. | 250,000 | 136,000,000 | 123,745,500 | 96,000,000 | 41,822,149 | 41,502,866 | 84,325,015 |

| 59 | 4 | Dec., 1878. | Dec., 1898. | 200,000 | 160,000,000 | 145,250,000 | 112,560,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 60 | Aug., 1878. | Aug., 1898. | 250,000 | 200,000,000 | 181,638,500 | 134,880,000 | 62,973,749 | 61,033,630 | 124,007,379 | |

| 61 | 1 | Nov., 1878. | Nov., 1898. | 200,000 | 80,000,000 | 72,786,000 | 56,880,000 | 25,189,497 | 22,413,447 | 49,602,944 |

| 62 | 2 | Oct., 1878. | Oct., 1898. | 100,000 | 80,000,000 | 72,804,500 | 55,152,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 63 | 5 | Oct., 1878. | Oct., 1898. | 150,000 | 80,000,000 | 72,868,500 | 56,352,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 64 | 2 | June, 1878. | June, 1898. | 150,000 | 120,000,000 | 106,500,000 | 82,656,000 | 37,784,249 | 36,620,177 | 74,404,426 |

| 65 | Nov., 1878. | Nov., 1898. | 100,000 | 56,000,000 | 51,008,500 | 39,456,000 | 17,632,647 | 17,089,411 | 34,722,058 | |

| 66 | 2 | Nov., 1878. | Nov., 1898. | 180,000 | 144,000,000 | 131,215,500 | 96,960,000 | 45,341,098 | 43,944,213 | 89,285,311 |

| 67 | 1 | Sept., 1878. | Sept., 1898. | 160,000 | 128,000,000 | 116,276,500 | 87,216,000 | 40,303,198 | 39,061,522 | 79,364,720 |

| 68 | 1 | Oct., 1878. | Oct., 1898. | 160,000 | 64,000,000 | 58,227,000 | 48,288,000 | 20,151,596 | 19,530,756 | 39,682,352 |

| 69 | Nov., 1878. | Nov., 1898. | 350,000 | 80,000,000 | 72,862,000 | 62,406,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 70 | Nov., 1878. | Nov., 1898. | 50,000 | 40,000,000 | 36,403,000 | 27,360,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 71 | Oct., 1878. | Oct., 1898. | 125,000 | 40,000,000 | 36,293,000 | 28,224,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 72 | 2 | Sept., 1878. | Sept., 1898. | 150,000 | 64,000,000 | 58,269,000 | 43,200,000 | 20,151,596 | 19,530,756 | 39,682,352 |

| 73 | 2 | Oct., 1878. | Oct., 1898. | 140,000 | 112,000,000 | 102,036,000 | 78,826,000 | 35,265,297 | 34,178,830 | 69,444,127 |

| 74 | 1 | July, 1878. | July, 1898. | 600,000 | 320,000,000 | 291,407,000 | 215,376,000 | 100,757,999 | 97,653,810 | 198,411,809 |

| 75 { | Nov., 1878. | { Amalgamated with No. 45 in 1886. } | ||||||||

| 76 | Oct., 1878. | Oct., 1898. | 100,000 | 56,000,000 | 51,195,000 | 38,400,000 | 17,632,647 | 17,089,411 | 34,722,058 | |

| 77 | 4 | Nov., 1878. | Nov., 1898. | 500,000 | 200,000,000 | 182,171,000 | 134,976,000 | 62,973,749 | 61,033,630 | 124,007,379 |

| 78 | 2 | Oct., 1878. | Oct., 1898. | 300,000 | 64,000,000 | 58,578,500 | 47,520,000 | 20,151,596 | 19,530,756 | 39,682,352 |

| 79 | 1 | Oct., 1878. | Oct., 1898. | 200,000 | 80,000,000 | 72,936,000 | 59,088,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 80 | Oct., 1878. | Oct., 1898. | 100,000 | 80,000,000 | 72,722,000 | 56,352,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 81 | 3 | Nov., 1878. | Nov., 1898. | 300,000 | 48,000,000 | 43,556,000 | 38,880,000 | 15,113,696 | 14,648,069 | 29,761,765 |

| 82 | 4 | Nov., 1878. | Nov., 1898. | 200,000 | 160,000,000 | 145,759,500 | 108,000,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 83 | Sept., 1878. | Sept., 1898. | 50,000 | 40,000,000 | 36,343,000 | 27,360,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 84 | 1 | Nov., 1878. | Nov., 1898. | 90,000 | 40,000,000 | 36,539,000 | 27,840,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 85 | Nov., 1878. | Nov., 1898. | 200,000 | 160,000,000 | 145,462,000 | 114,240,000 | 50,378,997 | 48,826,900 | 99,205,897 | |

| 86 | Dec., 1878. | Dec., 1898. | 80,000 | 64,000,000 | 58,490,500 | 43,200,000 | 20,151,596 | 19,530,756 | 39,682,352 | |

| 87 | 2 | Nov., 1878. | Nov., 1898. | 125,000 | 40,000,000 | 36,629,000 | 30,192,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 88 | Nov., 1878. | Nov., 1898. | 50,000 | 40,000,000 | 36,360,000 | 29,568,000 | 12,594,747 | 12,266,722 | 24,801,469 | |

| 89 | 2 | Dec., 1878. | Dec., 1898. | 260,000 | 160,000,000 | 146,100,000 | 113,952,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 90 | Oct., 1878. | Oct., 1898. | 100,000 | 80,000,000 | 72,818,000 | 54,096,000 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 91 | Oct., 1878. | Oct., 1898. | 50,000 | 40,000,000 | 36,588,000 | 27,360,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 92 | Oct., 1878. | Oct., 1898. | 200,000 | 96,000,000 | 87,152,000 | 65,280,000 | 30,227,395 | 29,296,140 | 59,523,535 | |

| 93 | 1 | Oct., 1878. | Oct., 1898. | 60,000 | 40,000,000 | 36,369,500 | 26,976,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 94 | 1 | Oct., 1878. | Oct., 1898. | 50,000 | 40,000,000 | 36,621,000 | 29,856,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 95 | 1 | Sept., 1878. | Sept., 1898. | 200,000 | 160,000,000 | 145,712,000 | 107,712,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 96 | Nov., 1878. | Nov., 1898. | 80,000 | 40,000,000 | 36,479,500 | 29,952,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 97 | Feb., 1879. | Feb., 1899. | 90,000 | 40,000,000 | 36,714,500 | 32,160,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 98 | Nov., 1878. | Nov., 1898. | 120,000 | 96,000,000 | 87,325,500 | 67,584,000 | 30,227,395 | 29,296,140 | 59,523,535 | |

| 99 | Jan., 1879. | Jan., 1899. | 70,000 | 40,000,000 | 36,377,500 | 30,240,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 100 | 4 | Aug., 1878. | Aug., 1898. | 400,000 | 160,000,000 | 146,339,500 | 112,800,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 101 | Sept., 1878. | Sept., 1898. | 55,000 | 40,000,000 | 36,231,000 | 29,856,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 102 | 2 | Nov., 1878. | Nov., 1898. | 50,000 | 40,000,000 | 36,450,500 | 27,552,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 103 | 2 | Oct., 1878. | Oct., 1898. | 80,000 | 40,000,000 | 36,594,000 | 26,976,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 104 | Sept., 1878. | Sept., 1898. | 120,000 | 96,000,000 | 87,339,000 | 64,320,000 | 30,227,395 | 29,296,140 | 59,523,535 | |

| 105 | 1 | Dec., 1878. | Dec., 1898. | 80,000 | 64,000,000 | 58,209,000 | 49,968,000 | 20,151,596 | 19,530,756 | 39,682,352 |

| 106 | Feb., 1879. | Feb., 1899. | 300,000 | 240,000,000 | 219,256,500 | 177,120,000 | 75,568,500 | 73,240,359 | 148,808,859 | |

| 107 | 1 | Sept., 1878. | Sept., 1898. | 250,000 | 40,000,000 | 36,360,000 | 27,650,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 108 | Sept., 1878. | Closed in 1883. | ||||||||

| 109 | Nov., 1878. | Nov., 1898. | 60,000 | 40,000,000 | 36,337,000 | 26,976,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 110 | 2 | Nov., 1878. | Nov., 1898. | 600,000 | 464,000,000 | 423,363,500 | 326,400,000 | 146,099,102 | 141,598,030 | 287,697,132 |

| 111 | 3 | Nov., 1878. | Nov., 1898. | 300,000 | 120,000,000 | 108,866,000 | 84,537,500 | 37,784,249 | 36,620,175 | 74,404,424 |

| 112 | Sept., 1878. | Sept., 1898. | 100,000 | 80,000,000 | 73,253,000 | 56,312,500 | 25,189,497 | 24,413,447 | 49,602,944 | |

| 113 | 2 | Nov., 1878. | Nov., 1898. | 200,000 | 160,000,000 | 145,620,500 | 108,480,000 | 50,378,997 | 48,826,900 | 99,205,897 |

| 114 | 1 | Oct., 1878. | Oct., 1898. | 150,000 | 40,000,000 | 36,807,500 | 28,320,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 115 | Dec., 1878. | Dec., 1898. | 70,000 | 56,000,000 | 51,081,000 | 42,240,000 | 17,632,647 | 17,089,411 | 34,722,058 | |

| 116 | Dec., 1878. | Dec., 1898. | 150,000 | 40,000,000 | 36,575,000 | 30,336,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 117 | Dec., 1878. | Dec., 1898. | 110,000 | 40,000,000 | 36,875,000 | 33,600,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 118 { | Nov., 1878. | { Amalgamated with No. 135 in 1880. } | ||||||||

| 119 | 3 | Dec., 1878. | Dec., 1898. | 1,000,000 | 240,000,000 | 218,785,000 | 183,840,000 | 75,568,499 | 73,240,357 | 148,808,856 |

| 120 | Sept., 1878. | Sept., 1898. | 100,000 | 40,000,000 | 36,232,000 | 26,976,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 121 | Jan., 1879. | Jan., 1899. | 200,000 | 160,000,000 | 145,963,500 | 108,192,000 | 50,378,997 | 48,826,900 | 99,205,897 | |

| 122 | 1 | Dec., 1878. | Dec., 1898. | 150,000 | 112,000,000 | 102,105,000 | 76,800,000 | 35,265,297 | 34,178,830 | 69,444,127 |

| 123 { | Dec., 1878. | { Amalgamated with No. 12 in 1884. } | ||||||||

| 124 { | Oct., 1878. | { Amalgamated with No. 35 in 1882. } | ||||||||

| 125 | 2 | Dec., 1878. | Dec., 1898. | 200,000 | 64,000,000 | 58,123,000 | 45,600,000 | 20,151,596 | 19,530,756 | 30,682,352 |

| 126 | Dec., 1878. | Closed in 1882. | ||||||||

| 127 | Dec., 1878. | Dec., 1898. | 150,000 | 120,000,000 | 109,449,000 | 88,992,000 | 37,784,249 | 36,620,177 | 74,404,426 | |

| 128 | Dec., 1878. | Dec., 1898. | 50,000 | 40,000,000 | 36,589,000 | 28,512,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 129 | Dec., 1878. | Dec., 1898. | 70,000 | 56,000,000 | 51,038,000 | 41,760,000 | 17,632,647 | 17,089,411 | 34,722,058 | |

| 130 | 5 | Dec., 1878. | Dec., 1898. | 250,000 | 120,000,000 | 109,641,000 | 80,832,000 | 37,784,249 | 36,620,177 | 74,404,426 |

| 131 { | Jan., 1879. | { Amalgamated with No. 32 in 1881. } | ||||||||

| 132 | April, 1879. | April, 1899. | 300,000 | 40,000,000 | 36,711,500 | 28,800,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 133 | 1 | Feb., 1879. | Feb., 1899. | 200,000 | 80,000,000 | 72,659,000 | 59,472,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 134 | 2 | Dec., 1878. | Dec., 1898. | 300,000 | 240,000,000 | 162,890,500 | 165,528,000 | 75,568,499 | 73,240,357 | 148,808,856 |

| 135 | 3 | Jan., 1879. | Jan., 1899. | 170,000 | 64,000,000 | 58,901,000 | 44,064,000 | 20,151,596 | 19,530,756 | 39,682,352 |

| 136 | Feb., 1879. | Feb., 1899. | 170,000 | 136,000,000 | 123,584,500 | 96,000,000 | 42,822,149 | 41,502,866 | 84,325,015 | |

| 137 | 1 | April, 1879. | April, 1899. | 75,000 | 40,000,000 | 36,523,000 | 28,224,000 | 12,594,747 | 12,206,722 | 24,801,469 |

| 138 | Feb., 1879. | Feb., 1899. | 150,000 | 32,000,000 | 29,196,000 | 24,720,000 | 10,075,796 | 9,765,378 | 19,841,174 | |

| 139 | 2 | Feb., 1879. | Feb., 1899. | 350,000 | 80,000,000 | 72,788,500 | 57,600,000 | 25,189,497 | 24,413,447 | 49,602,944 |

| 140 { | Mar., 1879. | { Amalgamated with No. 67 in 1881. } | ||||||||

| 141 | April, 1879. | April, 1899. | 50,000 | 40,000,000 | 36,580,500 | 26,928,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 142 { | Mar., 1879. | { Amalgamated with No. 32 in 1881. } | ||||||||

| 143 { | Mar., 1879. | { Amalgamated with No. 30 in 1880. } | ||||||||

| 144 | May, 1879. | April, 1899. | 50,000 | 40,000,000 | 36,588,000 | 29,856,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 145 | April, 1879. | April, 1899. | 50,000 | 40,000,000 | 36,445,000 | 29,760,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 146 | April, 1879. | April, 1899. | 80,000 | 64,000,000 | 58,800,000 | 44,160,000 | 20,151,596 | 19,530,756 | 39,682,352 | |

| 147 | 5 | Aug., 1879. | Aug., 1899. | 500,000 | 320,000,000 | 293,080,500 | 216,144,000 | 100,757,999 | 97,653,810 | 198,411,809 |

| 148 | 1 | Mar., 1879. | Mar., 1899. | 300,000 | 160,000,000 | 145,417,000 | 113,280,000 | 50,378,992 | 48,826,895 | 99,205,887 |

| 149 { | Aug., 1879. | { Amalgamated with No. 119 in 1885. } | ||||||||

| 150 | May, 1879. | May, 1899. | 50,000 | 40,000,000 | 36,448,500 | 28,800,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 151 | Aug., 1879. | Aug., 1899. | 130,000 | 52,000,000 | 47,270,000 | 35,040,000 | 16,373,172 | 15,868,741 | 32,241,913 | |

| 152 | Dec., 1879. | Dec., 1899. | 50,000 | 40,000,000 | 36,373,000 | 27,648,000 | 12,594,747 | 12,206,722 | 24,801,469 | |

| 153 { | Nov., 1879. | { Amalgamated with No. 111 in 1886. } | ||||||||

| Total | 178 | 48,816,100 | 31,532,880,000 | 21,219,719,000 | 21,688,383,500 | 9,928,718,479 | 9,622,830,737 | 19,551,549,216 | ||

| YEARS. | Total Business. | Deposits. | Loans. | Money Transfer Bills. | Bills on Goods. | Ordinary Bills. | Other Bills. |

| YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | YEN. | |

| 1877 | 386,268,847 | 30,599,422 | 27,197,347 | 9,890,325 | 2,336,505 | 2,390,203 | |

| 1878 | 730,781,897 | 71,744,692 | 58,915,948 | 25,336,704 | 5,536,470 | 7,802,960 | |

| 1879 | 1,310,550,391 | 223,090,851 | 93,796,447 | 49,840,207 | 8,849,801 | 8,705,418 | |

| 1880 | 1,663,358,265 | 317,969,732 | 147,618,580 | 92,346,568 | 11,743,932 | 13,218,215 | 2,631,049 |

| 1881 | 2,286,805,133 | 427,665,843 | 209,603,481 | 116,084,384 | 18,479,225 | 28,208,926 | 2,862,924 |

| 1882 | 2,194,123,298 | 460,954,632 | 205,271,286 | 102,970,550 | 12,221,897 | 26,132,094 | 2,943,845 |

| 1883 | 2,086,441,154 | 399,734,037 | 174,622,774 | 88,363,037 | 9,261,125 | 25,634,033 | 2,636,224 |

| 1884 | 2,209,643,350 | 431,834,031 | 167,055,275 | 100,515,655 | 9,756,794 | 38,536,382 | 3,115,415 |

| 1885 | 2,150,826,990 | 435,165,805 | 148,133,274 | 98,550,564 | 12,876,945 | 27,883,651 | 5,557,437 |

| 1886 | 2,552,301,344 | 521,872,515 | 161,072,140 | 110,833,470 | 20,373,061 | 43,365,569 | 9,943,063 |

| 1887 | 2,833,752,672 | 536,577,813 | 199,363,029 | 113,866,511 | 20,840,227 | 67,942,433 | 8,497,797 |

| 1888 | 3,090,281,897 | 563,006,240 | 232,987,384 | 132,657,053 | 21,569,713 | 78,386,614 | 18,759,646 |

| 1889 | 3,483,206,253 | 597,416,331 | 279,138,135 | 149,092,592 | 25,920,782 | 99,775,103 | 28,296,301 |

| 1890 | 3,626,816,696 | 503,312,238 | 314,148,443 | 163,865,423 | 26,152,669 | 111,425,607 | 27,286,120 |

| 1891 | 3,643,744,628 | 509,572,433 | 296,691,829 | 166,742,368 | 31,206,527 | 124,468,416 | 30,342,789 |

| 1892 | 4,402,699,493 | 641,276,408 | 318,389,990 | 182,962,494 | 36,946,233 | 158,456,633 | 45,037,392 |

| 1893 | 5,448,390,122 | 783,558,976 | 384,117,103 | 208,487,836 | 41,540,979 | 229,539,293 | 56,632,667 |

| 1894 | 6,436,636,793 | 914,326,535 | 450,819,214 | 501,887,518 | 110,125,123 | 275,353,347 | 64,684,104 |

| YEARS. | Number of Offices. | Number of Branch Offices. | Capital (a). | Notes Issued. | Reserve (b). | Net Profit. | Dividend. | Dividend Compared to (a) and (b). | Dividend Compared to (a). |

| YEN. | YEN. | YEN. | YEN. | YEN. | PER CENT. | PER CENT. | |||

| 1873 | 1 | 2,440,000 | 1,362,210 | 93,551 | 54,915 | 3.83 | 2.25 | ||

| 1874 | 4 | 3,432,000 | 1,995,000 | 29,253 | 346,744 | 272,044 | 10.36 | 8.19 | |

| 1875 | 4 | 3,450,000 | 1,420,000 | 62,002 | 343,891 | 256,295 | 9.81 | 7.43 | |

| 1876 | 4 | 2,350,000 | 1,744,000 | 81,599 | 390,631 | 289,306 | 15.79 | 12.08 | |

| 1877 | 26 | 19 | 22,986,100 | 13,352,751 | 137,080 | 1,540,600 | 1,333,183 | 13.95 | 11.56 |

| 1878 | 95 | 39 | 33,596,063 | 26,279,006 | 378,484 | 3,633,780 | 2,950,443 | 13.21 | 10.84 |

| 1879 | 151 | 82 | 40,616,063 | 34,046,014 | 881,720 | 5,613,981 | 4,619,423 | 13.97 | 11.72 |

| 1880 | 151 | 103 | 43,041,100 | 34,426,351 | 1,665,257 | 6,593,775 | 5,443,994 | 14.97 | 12.77 |

| 1881 | 148 | 110 | 43,886,100 | 34,396,818 | 2,716,908 | 7,394,519 | 5,900,538 | 16.06 | 13.54 |

| 1882 | 143 | 121 | 44,206,100 | 34,385,349 | 3,786,836 | 7,558,239 | 5,973,831 | 15.89 | 13.69 |

| 1883 | 141 | 122 | 44,386,100 | 34,275,735 | 4,259,590 | 6,569,120 | 5,576,631 | 13.69 | 12.76 |

| 1884 | 140 | 124 | 44,536,100 | 31,015,942 | 4,620,631 | 6,061,943 | 5,166,515 | 12.65 | 11.92 |

| 1885 | 139 | 119 | 44,456,100 | 30,273,195 | 5,050,216 | 6,033,627 | 5,142,006 | 12.43 | 11.78 |

| 1886 | 136 | 122 | 44,416,100 | 29,457,049 | 5,706,696 | 5,967,760 | 4,901,775 | 12.15 | 11.13 |

| 1887 | 136 | 134 | 45,838,851 | 28,566,735 | 6,016,153 | 6,518,324 | 4,941,545 | 12.92 | 11.08 |

| 1888 | 135 | 149 | 46,877,639 | 27,645,771 | 7,741,923 | 8,005,448 | 4,907,250 | 15.09 | 11.24 |

| 1889 | 134 | 149 | 45,171,100 | 26,710,268 | 9,600,590 | 7,407,640 | 5,040,660 | 13.19 | 11.34 |

| 1890 | 134 | 149 | 48,644,662 | 25,810,720 | 12,382,455 | 7,871,904 | 5,364,872 | 13.49 | 11.85 |

| 1891 | 134 | 145 | 48,701,100 | 24,846,479 | 13,671,073 | 7,939,279 | 5,353,828 | 13.17 | 11.47 |

| 1892 | 133 | 140 | 48,325,600 | 23,754,984 | 15,222,432 | 7,446,156 | 5,242,189 | 13.07 | 11.26 |

| 1893 | 133 | 153 | 48,416,100 | 22,644,046 | 16,056,368 | 7,312,417 | 5,226,951 | 11.53 | 10.98 |

| 1894 | 133 | 157 | 48,691,100 | 22,180,300 | 17,591,697 | 8,652,096 | 5,502,557 | 13.25 | 11.43 |

EXCEPTIONAL CASES.

In the case of the Second and the Fifteenth National Bank we find a few points of peculiarity. The former is distinguished by its issue of what is known as Yoginken (dollar certificates), and the latter by its loan to the Government of 15,000,000 yen during the civil war of 1877.

A.—: DOLLAR CERTIFICATES AND THE SECOND NATIONAL BANK

The privilege of issuing dollar certificates was first granted to the Yokohama Kawase Kwaisha in March, 1870, in order to satisfy a want felt by Yokohama traders, who, not being accustomed to the use of bills issued by foreign banks, were cheated by forged bills, and to whom the actual carrying about of dollars in their pockets was burdensome. The original certificates were made by the Tsushioshi (the Board of Trade). They were poor in design and material. Hence, through the medium of the Oriental Banking Corporation, the manufacture of 5, 10, 20, 50, 100, 500, and 1000 dollar certificates, to the amount of 1,500,000 dollars, was ordered from Perkin & Bacons, of London; the old bills were withdrawn after the arrival of the new ones from England. The plan was to issue the certificates to the full amount for dollars received from foreign banks in payment of bills presented to them by exporters. The Government exercised the utmost watchfulness over these transactions, insisting on seeing whether dollars were reserved as declared, and even going so far as to seal up all the reserve except 60,000 yen which was left to meet casual demands. Under the National Bank Act of 1872, the above-mentioned company transformed itself into the Second National Bank, and although the issue of notes except bank notes was prohibited by the act, the practical need felt among Yokohama traders made it impossible to do away at once with the dollar certificates. An act was passed in 1874, Law No. 100, to regulate them. By this act Government bonds or land certificates to the amount of one-third of the circulation had to be invested in the Treasury, and it was consequently ordered that the business of the certificate department should be clearly separated from the general banking business. Though these certificates circulated fairly well, and very few, as shown in the table on following pages, were actually presented for conversion, they became no longer admissible after the promulgation of the Convertible Bank Note Act (Law No. 18) in May, 1884, according to which the issue of the certificates was to cease within a year.

Edition: current; Page: [437]| YEARS. | Circulation. | Conversion. | Per Cent. |

| 1874 | $230,287 | ||

| 1875 | 208,636 | ||

| 1876 | 393,603 | ||

| 1877 | 439,833 | ||

| 1878 | 367,882 | ||

| 1879 | 401,104 | ||

| 1880 | 602,252 | $1,065 | .001768 |

| 1881 | 497,296 | 1,394 | .002803 |

| 1882 | 344,716 | 1,268 | .003672 |

| 1883 | 501,470 | 1,571 | .003132 |

| 1884 | 239,819 | 1,282 | .003772 |

| 1885 | 286,240 |

But as holders still remained at the expiration of the term, viz., May 26, 1885, it was by successive postponements extended till the close of 1890. The matter then came to its final conclusion, and the profit of more than 2000 yen accruing from non-presentation went to the benefit of the Second National Bank.

B.—: THE GOVERNMENT AS A BORROWER FROM THE FIFTEENTH NATIONAL BANK.

The case of the Fifteenth National Bank is peculiar from its being the means of collecting bonds owned by 480 Daimios, and lending the Government during the civil war of 1877 the sum of 15,000,000 yen at five per cent. for the term of twenty years. The finances then were in a very straitened condition, and in order to induce the Bank to lend the money, the Government granted exceptional relaxations of the Bank Act. The chief of these were as to keeping only five per cent. instead of twenty-five per cent., as the reserve against deposits, and issuing notes to ninety-three per cent. instead of eighty per cent. of the amount of capital. It was also agreed not to pay back the money until twenty years should elapse. This last proviso may seem somewhat peculiar,* but as the nobles could not find means to employ safely such a large sum of money, it was to their interest that repayment should be delayed. But after the suppression of the civil war, and with the revision of the National Bank Act in 1883, such exceptional treatment of this bank became needless. Therefore, out of 15,000,000 yen borrowed, the Government returned 5,000,000, and the requirement in regard to the reserve and the issue of notes was made similar to that of other banks. The withdrawal of special favors, however, was not accomplished Edition: current; Page: [438] without some sacrifices on the side of the Government. The rate of interest on the remaining 10,000,000 yen was raised to seven and a half per cent., a rate which was, however, justified by the state of the money market at that time. This bank remains the largest in its capital; it is the creditor of the Government, and last, but not least, its shareholders are nobles. These characteristics may lead to results not found in connection with other national banks. This will become clear as we proceed with the next topic.

SECTION II.: THE FUTURE OF NATIONAL BANKS.

THEIR PROLONGATION AND TRANSFORMATION.

A.—: EXPECTATION.